$1,600,000 Settlement for the Wrongful Death of a Pedestrian

Butler | Kahn recently obtained a $1,600,000 settlement for our client whose father was killed while walking in a parking lot. The settlement reflects the full policy limits of the at-fault driver’s automobile and umbrella insurance policies, plus applicable underinsured motorist (“UM”) coverage.

Here’s more about the case.

Facts of the Collision

One afternoon, Mr. Phillips* was walking into his local grocery store when the unimaginable happened. An elderly driver attempted to back out of a parking spot but mistook the gas pedal for the brake. The driver backed into Mr. Phillips and did not stop driving. It was not until the driver’s car hit a pole (actually, a “bollard”) that the vehicle stopped.

Diagram of accident from police report.

Tragically Mr. Phillips died as a result of the collision.

Investigation into Pedestrian Death

Once our client hired us, we got to work investigating Mr. Phillips’ death. We knew Mr. Phillips was killed in a grocery store parking lot, which meant it was likely there was surveillance video. In order to ensure that the video was not deleted, we sent a preservation letter to the grocery store. This letter gave details of the incident (date, location, names) and asked the grocery store to preserve the video and make sure it was not deleted or written over. We also contacted the grocery store and requested a copy of any videos that recorded the incident. The grocery store then referred us to their loss prevention department. After multiple phone calls, we made contact with the loss prevention officer who had the video footage. Thankfully, he was willing to work with us and sent a copy of the video that recorded the incident. While the video was a bit blurry, it confirmed the elderly driver backed out of the parking spot at a high rate of speed, not stopping until he hit a bollard in front of the store.

Also, as part of our investigation, we did an Open Records Request seeking any reports, video, photos, and 911 calls. When an incident is still under investigation by the police, much of the evidence is not available to the public. When we sent our requests to the police department, their investigation was still pending, so we only received limited information. This limited information included a redacted incident report which listed the names of a few witnesses. As part of our investigation, we reached out to those witnesses. We were able to speak with two of them, but learned they only witnessed the events after the collision. This made us even more grateful for the surveillance video we obtained.

Insurance Investigation

As part of our investigation into Mr. Phillips’ death, we also needed to locate the available insurance. Most police reports contain drivers’ insurance policy numbers and the name of their insurance companies. The redacted report we received in response to our Open Records Request did have the elderly driver’s policy number and the name of his insurance company. In Georgia, you can send a request to an insurance company asking the insurance company to provide information for all known insurance policies that apply to an incident. See O.C.G.A. § 33-3-28. Unfortunately, the law allows an insurance company 60 days to respond.

In order to determine the policy limits quickly, we did a policy limits search through a third-party vendor. That search indicated that there was an insurance policy that applied to the wreck, but stated the elderly driver’s insurance limits only provided $25,000 in insurance coverage. (When the report shown below says “$25K/$50K,” that means that the limits are $25,000 per person and no more than $50,000 per collision – so here, since only one person was injured, the effective limits would have been $25,000.)

Snapshot of Third-Party Insurance Search

Since the limits were so low, we decided to file a lawsuit so we could make sure we could ask the elderly driver about any other policies of insurance he had. We were surprised to learn that the elderly driver actually had an auto insurance policy of $500,000 and, through a different insurer, an umbrella insurance policy of $1,000,000.

Mr. Phillips also had his own underinsured motorist (“UM”) coverage through his car insurance. Through a request pursuant to O.C.G.A. § 33-3-28, we learned his policy provided $100,000 of coverage. Pursuant to O.C.G.A. § 33-7-11, that UM coverage applied to our wrongful death case, even though the decedent was a pedestrian, because the death “arose from” the use of a motor vehicle.

What is a Wrongful Death Claim?

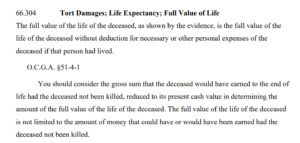

When someone is killed as a result of someone else’s negligence, a person’s family can bring a wrongful death claim. In Georgia, the victim’s family can make a claim for “the full value of the life of the decedent.” O.C.G.A. § 51-4-2. Georgia’s pattern jury instruction 66.304 (which is the instruction a judge gives a jury before a jury deliberates) explains what a jury should consider when awarding money for the full fall value of the life of the victim:

Only the victim’s surviving spouse, children, and parents can sue for wrongful death unless the victim has no surviving family members. If the victim has no surviving family members, a personal representative may file a wrongful death lawsuit on behalf of the victim’s estate.

Mr. Phillips did not have a spouse but had one child. Because of this, Mr. Phillips’ child had the right to bring the wrongful death claim against the elderly driver.

What is an estate claim?

When someone is killed as a result of someone else’s negligence, there is also an “estate claim.” The estate claim allows recovery for the pain and suffering of the victim, any medical bills incurred before death, funeral expenses, punitive damages, and other necessary expenses. O.C.G.A.§ 51-4-5.

This estate claim is brought by the representative of the victim’s estate. Often (but not always), this representative is the same person who has the right to bring the wrongful death claim (i.e. a surviving spouse or surviving child). If the victim had a will, then the administrator named in the will must bring the estate claim. If the victim did not have a will, then Georgia’s rules of inheritance laid out in O.C.G.A. § 53-2-1 explains who has the right to bring the claim.

Because Mr. Phillips did not have a will or a surviving spouse, his surviving child was able to bring the estate claim against the elderly driver. In order to formally appoint his child as the representative of his estate, we worked with a probate attorney to file a “Petition for Letters of Administration.” Letters of Administration are the formal documents a probate court grants the estate’s representative. These Letters allow the representative to handle affairs on behalf of the victim’s estate, including suing the negligent party.

Copy of signed Letters of Administration

$1,600,000 Wrongful Death of a Pedestrian Settlement

Through our investigation, we learned there was a total of $1,600,000 in insurance coverage for the wreck. There was $500,000 from the driver’s auto insurance, $1,000,000 from the driver’s umbrella insurance, and $100,000 from Mr. Phillips’ UM insurance. We made a policy-limits offer to the elderly driver’s insurance companies to settle the claims arising from Mr. Phillips’ death and the companies accepted our offer. We also sent a policy-limits demand to Mr. Phillips’ insurance company, and it also accepted our offer. That led to the total settlement of $1,600,000 in this wrongful death case.

Through our investigation, we learned there was a total of $1,600,000 in insurance coverage for the wreck. There was $500,000 from the driver’s auto insurance, $1,000,000 from the driver’s umbrella insurance, and $100,000 from Mr. Phillips’ UM insurance. We made a policy-limits offer to the elderly driver’s insurance companies to settle the claims arising from Mr. Phillips’ death and the companies accepted our offer. We also sent a policy-limits demand to Mr. Phillips’ insurance company, and it also accepted our offer. That led to the total settlement of $1,600,000 in this wrongful death case.

While no amount of money will ever make up for the loss of Mr. Phillips’ life, our client was pleased with the results.

*This name and the names of other involved parties have been changed for privacy reasons.

- Apartment Shooting Settlement

- Bike Accident Settlement

- Boating Accident Settlement

- Boating Settlement Accident

- Car Accident Jury Verdict

- Car Accident Settlement

- Dog Bite

- Motorcycle Accident Settlement

- Negligent Security Shooting Settlement

- Pedestrian Accident Settlement

- Personal Injury Verdict

- Settlement in Sexual Assault Case

- Sexual Assault Verdict

- Truck Accident

- Wrongful Death Settlement

Contact Us Now

Contact Us Now

Lawrenceville, GA 30046

Jonesboro, GA 30236